Adyen: Looking Beneath the Headlines

Quality & growth runaway intact, but at a slower velocity than what many thought. High-teens IRR at conservative numbers in the long-term. Street oversimplifies headlines.

The first post will be an overview of the current Adyen situation & valuation from here. I will focus on the critical controversies around the story raised after the 1H23 results and talk about what’s key on the fundamental side. For a more comprehensive view of how processors like Adyen add value to their clients, please refer to my Online Enterprise Payments 101 post.

Quick Summary:

Volume miss in 1H23 was influenced mainly by weak underlying growth of top merchants and the eBay one-off churn rather than driven by competition

Headline comparison with Braintree’s growth is misleading; Adyen actually likely grew more dollars than Braintree in NAM after adjusting for eBay, SMB volumes, and merchants’ organic growth

Adyen’s 1H23’s weakness sat mostly within Adyen’s net new business side, which was likely competition-driven. However, net retention rates, partial churn, market-share gains, and take rates were strong globally and in North America (NAM). This combo is a much stronger indicator of a stable competitive edge than net new business performance in a short window, given the longer lead time (often 8+ months) required for Adyen to deliver its full value potential on domestic volumes

Adyen’s NAM net new business deceleration is fixable; Core NAM issue is being addressed by optimizing sales tactics toward interchange/authorization rate optimizations rather than functionality (e.g., payment methods, conversion, customer data, loyalty programs, omnichannel) and increasing the salesforce given the large market opportunity; Adyen’s commercial teams’ targets have been disproportionately focused on existing customers’ wallet expansion

Braintree’s bundling strategy, which hit Adyen’s new business somewhat, is unsustainable. This is because i) others, such as market-leader Chase, have tried it and proven it to be insufficient, and ii) PayPal can’t structurally afford it for long because the Button & Wallet are structurally losing share in a way PYPL’s cost base won’t be able to afford net losses from the acquiring business (breakeven acquiring take-rates are much higher than what’s been sold)

Adyen’s terminal take-rates should be much higher than what’s implied in the stock price because i) online take-rates will fundamentally settle at higher levels than what offline rates settled, and ii) Adyen’s premium service, in most cases, cover peer prices even if they were almost free, and its competitive edge should widen in the US going forward as scale increases and product matures with recently granted licenses

Long-term margins seem feasible - it is under management’s control. Recent hiring spree has significantly skewed toward tech, of which a good chunk has been into new products (much like Google’s “Other Bets”), which barely generate revenue. Normalized hiring should resemble pre-2022 absolute YoY levels

High-teens IRR by 2027 @ the ~€670/share entry-point seems achievable using conservative assumptions, significantly below management’s medium-term guidance; Entry point is tricky as consensus remains more optimistic than the buy-side ahead of Investor Day & Q3 Update

Detailed:

A strong net revenue retention at stable take rates means that partial churn is likely healthy

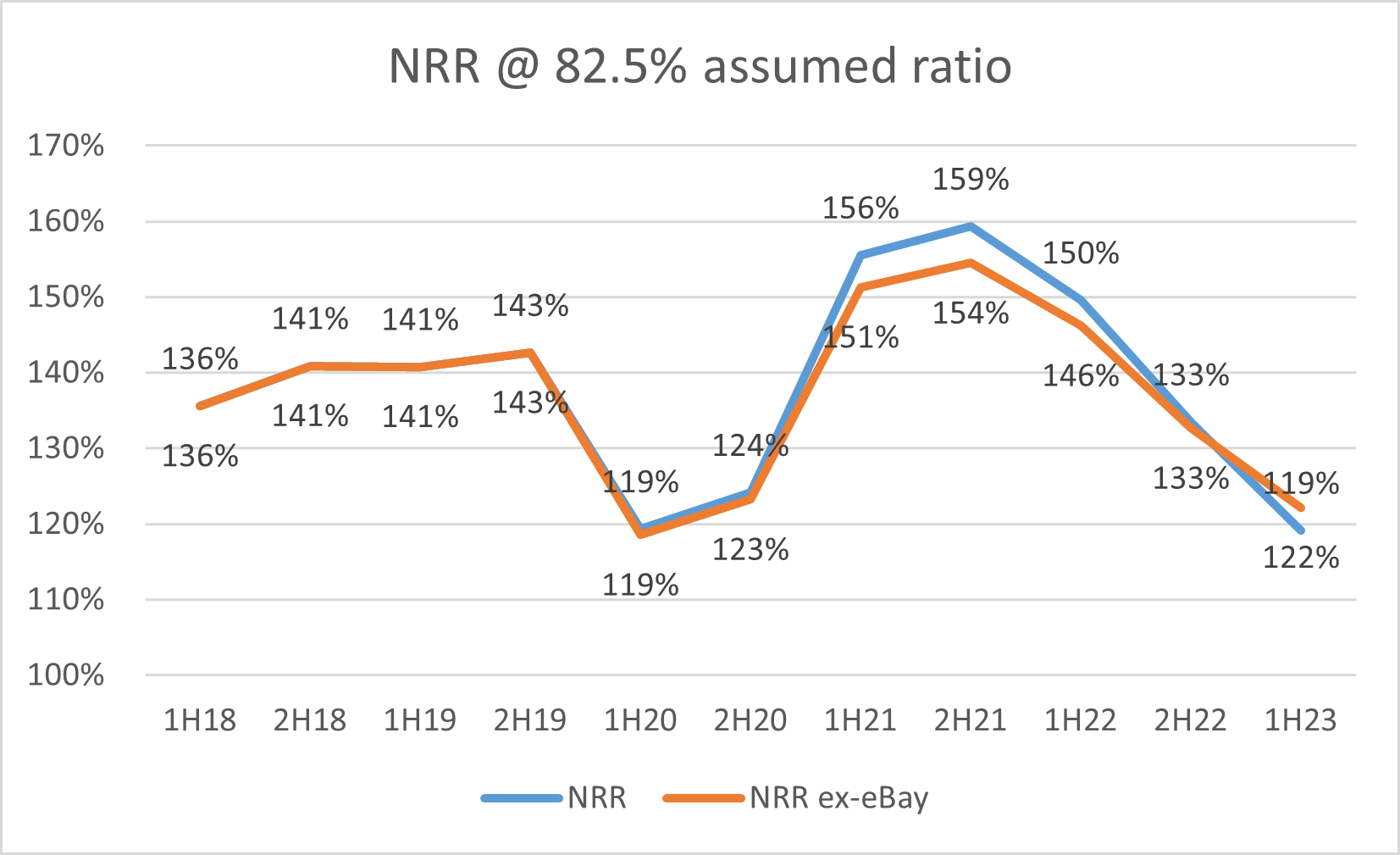

It is possible to have a reasonable estimation of Net Retention Rates as Adyen reports the approximate % of volume growth comes from existing customers. It’s been “>80%” since the IPO; if my checks with IR and others are right, it’s usually up to 85%. The residual <20% relates to growth attributed to new customers.

What deviated from past results this time was Adyen’s net new business. This growth portion is similar to the “Net New Annualized Recurring Revenue” or “NNARR” of subscription businesses. We can deem Adyen’s volumes “recurring” as Adyen reports that the churn of merchants that completely left the platform has been <1% in $ terms in every result since its IPO. The problem is that Adyen doesn’t report “partial” churn, the industry's most common type of churn.

When decent PSPs (payment service providers - acquirers, gateways, or both) underperform, they are most likely to be taken away from processing, e.g., 30% of a merchant's volume to 20%, 10%, or 5%. Most large merchants work with all the leading acquirers to some extent (e.g., backup reasons, suitability for specific payment methods, specific payment rails, regions, channels, etc.).

But what most investors don’t realize is that the way to get around unreported partial churn is to estimate Net Retention Rates, which incorporate partial churn, wallet-share gains, and organic/underlying merchant growth. If NRR is way above underlying growth and/or market growth, it’s less likely there’s been significant partial churn.

The eBay impact

Before diving into the numbers, it is important to clarify the growth impact in 1H23 from one of Adyen’s largest NAM merchants, eBay.

As part of the deal sealed in 2019, eBay finished migrating c.100% of its volumes to Adyen, from PayPal in the US by 1H22. In 1H23, though, Adyen reported that eBay had churned off some volumes from Adyen due to “natural optimizations” within certain payment methods. Later in the GS Conference, management clarified that the churn seen was that eBay simply chose to integrate directly with AmEx and PayPal (meaning using their processors on transactions done through those payment methods) rather than using Adyen, a movement that Adyen already expected. This is indeed relatively standard in the industry - most merchants use AmEx/PYPL processors in those transactions because they get significant rebates in the interchange fees, mainly in the US, where interchange costs more.

Adyen reported that the ex-eBay growth of its Platforms verticals was +82% YoY ex-Ebay, +3% including eBay. Per my calculations using past eBay disclosures, the overall churn from eBay means Adyen went from processing c.100% of eBay’s volumes in the US to c.63%. This is still at the high end of what the main acquirer tends to get from a large merchant. Large merchants that are large Adyen processors tend to rover around 40-60% of exposure to Adyen, so it isn’t indicative at all of decreased competitive advantage.

Overall, eBay was a c3pp drag in online TPV growth for 1H23 (c.17.4% YoY including, c.20.6% YoY excluding eBay).

IMO, Adyen’s management failed to communicate that this churn was a significant drag in the overall results & NAM segment growth. This aligns with management’s preference of not guiding/making caveats for single-merchant movements in earnings calls (mainly because this is messy, volatile, and sometimes confidential). However, given the size of the miss in this result, management should have explained it better.

Back to NRR…

With the eBay caveat in mind, let’s return to the NRR. Within an assumed range of 80-85% of growth from existing customers, 1H23 NRR therefore came at c119% - 121%, and NNARR came in at €16-€12B (c. -38% YoY).

If we exclude the impact from eBay volumes, NRR would be c2pp higher in 1H23. The table below shows the evolution of the NRR.

NRR is important as a proxy for competitive edge because merchants usually take 8-12+ months to fully reap the Adyen platform's and its team's value, especially for domestic-only volumes. Things like i) faster platform adaptation (vs. other processors) to network/scheme/issuer dynamic rules & products happen throughout the year, ii) consulting-like services such as interchange & conversion optimization need ongoing inputs from the Adyen team, iii) full integration of Adyen’s omnichannel strategy takes several months due to the inherently slow pace of POS switching, and iv) implementation of re-architecture products such as network tokens, new payment journeys (website / mobile / app integration and design, including new payment method adoption, loyalty programs, donation, etc.), token vaulting for non-PCI-compliant merchants, etc. also take time. This is different than the “value lead time” merchants get for global volumes, whereby simply switching to Adyen quickly results in instant bumps in authorization and conversion rates as a result of increased payment options, optimization of regulatory technologies (e.g., 3DS), local processing within different countries (skips many fees), FX adaptability, and better authorization rates given a highly complex web of banks / payment methods / payment rails that exist in Europe and APAC, especially. So, the customers who have already been with Adyen for a long time mean much more than the rate at which Adyen wins RFPs.

Importantly, we can only conclude that there are continued wallet-share gains as a result of the optical NRR to underlying growth / market growth delta because the cross-selling piece (i.e., non-payments products) for Adyen is still negligible. So, all the excess growth above market/customers’ is share-taking from other providers and does not include meaningful upsells from non-payment-processing products.

NNARR, on the other hand, can be more volatile. RFP win rates, a proxy for NNARR, favor the cost side of the equation in the current environment. If PayPal offers a 50bps overall take-rate discount relative to Adyen (often due to button-led interchange rebates), merchants cost-constrained for the year may go for PYPL so they can hit their cost targets because otherwise, they would have to spend months with Adyen to get the ROI that is not 100% guaranteed it comes fast enough. That’s basically what started to happen in 1H23, in my view. Cost has become a priority.

In this context, Adyen’s NRR levels are quite strong. This is especially because the underlying growth of Adyen’s main customers (SMB/B2C-Microsoft customers, FB/IG Ads / marketplace, Google Services, Netflix, etc.) was weak and had bad comps in 1H23. On a consolidated basis ex-airlines (full-stack & gateway ex-airlines - c90% of volumes), I estimate that the merchants had an underlying growth of only 6% YoY in 1H23 vs. 22% YoY in 1H22.

On the gateway side (c.20% of volumes), Adyen’s growth was similarly impacted by airlines' more muted organic growth (the bulk of gateway volumes). An aggregate of the top 20 publicly-listed airlines’ growth in 1H23 was c.4x lower than 1H22 - about the same ballpark as Adyen’s gateway growth decay (+107% YoY 1H22, +18% 1H23). It means the gateway side also performed in line with how much gateway customers consumed. [ Airline’s reported revenue growth is not ideally a proxy for Adyen’s gateway growth due to accounting & revenue model differences, so analyzing the degree of growth decay/accel works better ]

So, the c118% NRR (or c122% ex-eBay) means that Adyen outgrew the underlying growth of its customers’ piece by c3-4x, which aligns with its historical wallet-share gain pace.

The NRR number is likely even stronger in the US if we assume that the NNARR was proportionally weaker in the region, given the higher product sensitivity to macro conditions and the pricing pressure from PayPal (which I will discuss later below).

Finally, if we compare Adyen’s NRR gap to the overall market growth, as opposed to an estimation of its customer mix growth, we also see that Adyen posted a solid gap to the market.

Let’s assume NAM NRR was about the same as Total NRR, which is reasonable given Adyen’s net revenue growth in the US was 2pp higher than overall in 1H23. NAM ARR gap to the market was also sizable, as US e-commerce (about 50% of the online payments market) grew 7.5% YoY, and if we aggregate other verticals, the market grew about 10% in 1H23 (vs. Adyen’s NRR of 122% ex-eBay):

Be it through the NRR or net revenue performance lens, Adyen continued to gain a lot of share in NAM regardless of the weakness in new business seen in 1H23.

The conclusion would likely be the same by looking at EMEA and APAC, where growth was largely the same within key merchants and market-wise.

Hence, partial churn is likely not a problem given the strong NRR relative to organic client & market growth. Critically, stable net take rates reported in 1H23 corroborate it, as they don’t suggest that Adyen had to lower prices to keep its clients.

The composition of the market that I use stands as below (US$ bn):

Despite this current market structure, PSPs often have pretty different exposures to each subsegment. For example, Braintree’s exposure to the travel segment was about 10% pre-COVID, while Adyen’s was c30%. Adyen being a large Microsoft & Facebook processor means its exposure to digital ads and software might differ from a PSP who is not. This dynamic results in some difficulty in comparing PSP growth rates in windows where large verticals or pockets of merchants print uncommon growth. This happened in 2021 when Adyen’s growth rates were much higher than expected due to the resurgence of its travel vertical. It was one of the main reasons why consensus over-extrapolated growth rates in 2022 and 1H23. A similar situation is playing out for Adyen after the 1H23 - but to the under-estimation side.

Adyen’s NAM headline performance relative to Braintree was likely impacted in by an increased price-focused mentality from merchants but, above all, due to a few comparison nuances - eBay, BT’s merchant mix, and PPCP volumes

eBay was by far the most significant impact, responsible for c3pp to overall online full-stack TPV growth in 1H23, and c6pp for NAM full-stack TPV growth. Adyen's growth would be c.24.6% vs. 18.9% headline, against a low-30s headline growth for Braintree’s NAM.

In addition, Braintree’s PPCP business was responsible for $5B of volume growth in 2Q23, and I estimate $8B for 1H23. So, the +$40B number for total Braintree full-stack YoY growth in 1H23 should actually be $32B to better compare with Adyen’s. This is because PPCP’s customers are SMBs and do not represent volumes coming from large merchant wins. PPCP is a platform launched late last year that offers payment processing with customized checkout options, financing products, inventory management, and other tools to help SMBs manage their business. Those volumes that PPCP are converting are from SMBs ditching their acquirer processors to go with the whole suite from PayPal, effectively converting from gateway-only to full-stack clients on the processing side.

Finally, as showed earlier, end-market verticals in the US printed significant growth dispersion among them. For example, US ecomm grew 7.5%, while Food Delivery grew high-teens. Even more, there is dispersion within vertical themselves: if you’re a food delivery processor, you only fared well this half if you’d got DASH as a customer. Likewise for ridesharing, where Uber outgrew Lyft significantly.

PYPL is a large Uber and DoorDash processor in the US (while Adyen is not). Those merchants outgrew their peers in 1H23 in both the Food Delivery and Ridesharing verticals. As many expert calls have indicated, Uber and DASH can easily account for >20% of Braintree’s overall TPV in the US. Stronger growth from these guys favors Braintree.

Online Travel's leading players go mostly with non-Adyen processors for US volumes. Airbnb is not a big Adyen customer in the US and may have helped Braintree this half. Expedia is a significant Braintree customer and also outgrew the headlines.

In this context, it is fair to consider BT’s organic growth was c5pp higher than Adyen’s in 1H23 given the Uber/other exposures, but also due to eBay going back to Braintree to some extent. Assuming that c20% of eBay’s churn from Adyen went to Braintree (to take care of PYPL Button volumes), that would alone mean c1pp in extra organic growth for Braintree.

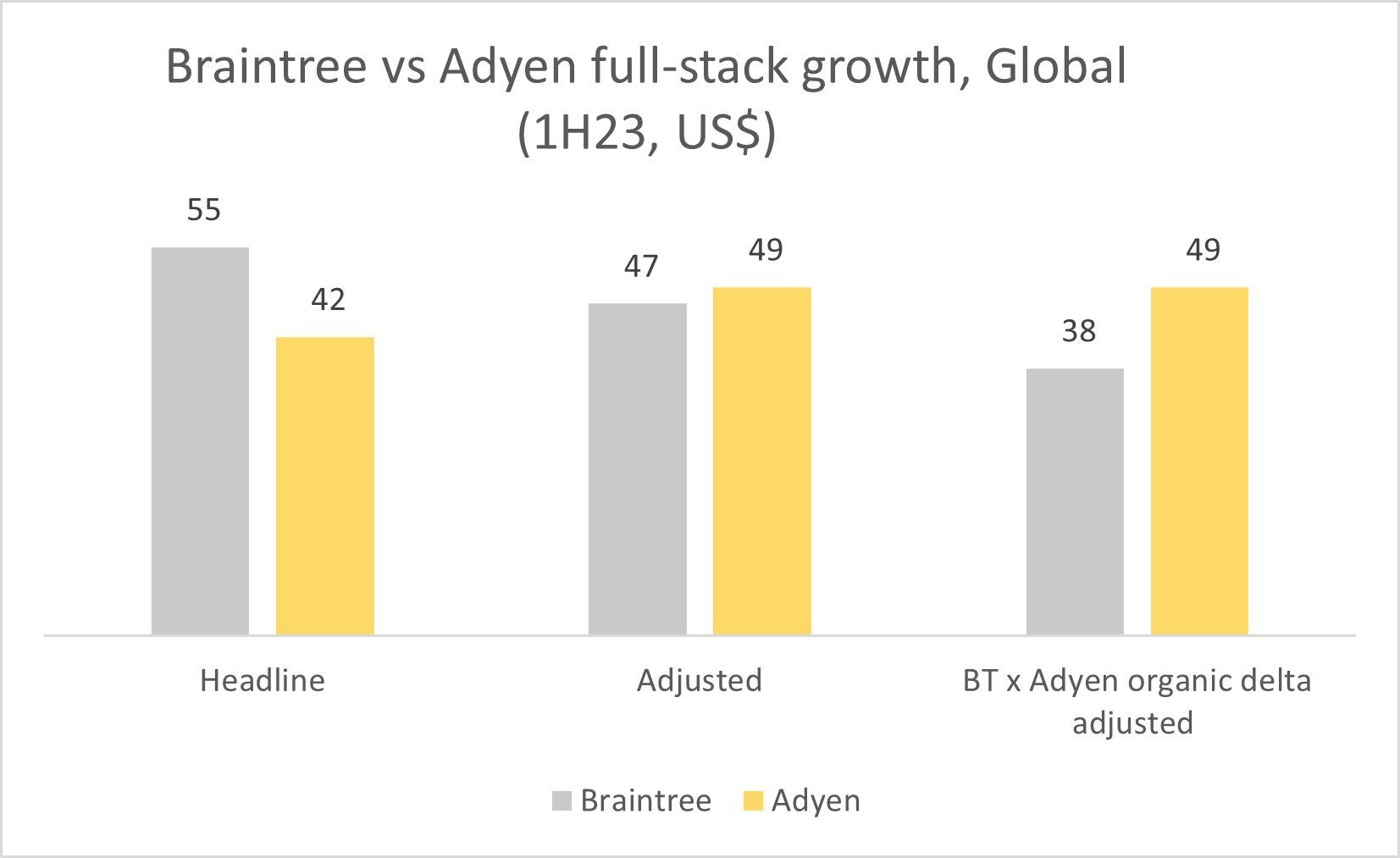

Here are a few snapshots of Adyen and Braintree's 1H23 full-stack growth comparison. First, I adjust BT for the PPCP effect and then for the c5pp higher organic growth differential vs. Adyen. Figures in US$ billions.

For Adyen, I adjusted volumes for the eBay impact.

Here, I compare the headline numbers, then the adjusted numbers for each (i.e. BT after PPCP, Adyen for eBay), and finally BT after PPCP & organic growth delta, vs. Adyen adj. for eBay.

We can see a wild gap in the headline vs. the final adjusted numbers, even if we ignore the organic growth adjustment. It tells us Adyen’s share-taking engine was actually fine in 1H23, both in NAM and Global.

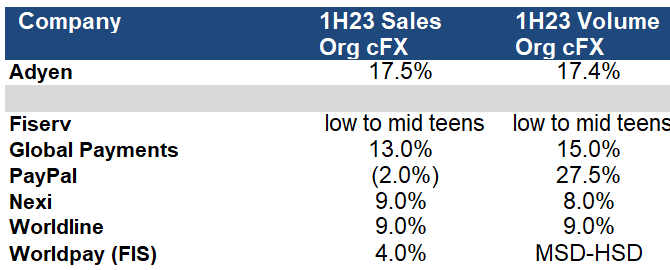

Here is the comparison in table form, including the non-full-stack number (i.e., including gateway-only numbers) and also growth figures from other processors in the same period (US$ bn):

We can further see that Adyen outperformed all peers above by a wide margin in 1H23. Notable absences in the table are Chase, where JPM’s management hasn’t commented on the business in the last earnings calls, and Stripe & Checkout (both private).

Here is a context of the recent growth of the main processors, where I calculate the market share of the leading acquirers by taking their TPV and dividing it by the sum of all the players’ TPVs:

[ I do this because key players such as Braintree, Stripe, GPN, and others use First Data and Chase as back-end processors - in the table below, First Data includes processing for PSPs and direct merchant processing, for example, so Chase/FD’s reported acquiring volumes would double-count its clients (e.g., Stripe) ]

Adyen has been clearly leading the pack. Legacy acquirers are religiously losing share. Braintree has shown some strength after 2020, Stripe (with a good chunk of SMB volumes) roughly at Braintree’s pace if we exclude Shopify (now churning off Stripe), and others barely moving the needle.

For the past year, Stripe & Checkout’s mentions within expert calls haven’t been called out competition-wise differently from the past, so I think it’s fair to assume they are not likely accelerating, given the past few years’ performances and recent layoffs / down rounds. On Chase, the last time management spoke about the business, they indicated the intent to increase value-added services. They are hopeful they can stabilize the market share after a re-engineering project that is about to finalize in a few years. Recent expert checks haven’t mentioned Chase being more aggressive on price or bundling than usual, consistent with the last 5-10 years. Who’s standing out this year is likely really Braintree.

I thought it would be helpful to take a broader view of the Adyen x Braintree NAM comparison by looking at more periods. Let’s look at 2020, which is when BT started increasing its market share again, which coincides with the final phases of the engineering overhaul they implemented after PayPal acquired it in 2013:

The gap between Adyen and Braintree has narrowed since 2022.

However, if we adjust for PPCP & the organic growth gap, Adyen has actually increased a bit from 2022 (1.3x vs. 1.1x). The 2021 difference was due to the travel segment - illustrating the difficulty in evaluating and extrapolating growth rates among payment peers again observed in a small reporting window. So, if we consider that the normalized gap between the two was an average over 2020-2022, the ratio would have been c1.6x in 1H23, compared to the c1.3x delivered by Adyen.

Adyen to BT ratio should have been 1.6x, ceteris paribus.

The c0.3x delta is likely primarily due to Adyen’s net new business underperformance, partially driven by BT pressure.

So, what’s happening at PayPal/Braintree?

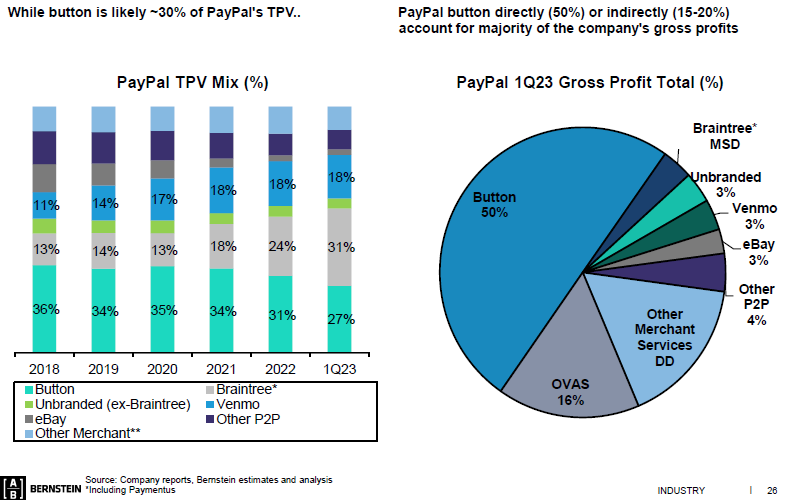

PayPal enjoys very deep economics in its core button business, where it gets a significant share of interchange fees along with Visa/Mastercard and issuer banks. PayPal button net take rates range from 1-2%, whereas net take rates for Braintree sit in the high single digits to mid-teens (e.g., 0.15%).

So, PayPal has three main ways to boost Braintree's acquiring volumes. First, it gives Braintree for free to merchants who commit to higher PayPal button checkout volumes (where it really makes money as a company – see below). Second, it negotiates better interchange rates for the merchant on PayPal Button volumes if the merchant commits to Braintree, which is especially advantageous in the US, where interchanges are higher. Third, it may enforce Braintree acquiring for the portion of the merchant’s transactions made using the PayPal Wallet.

PayPal button has c15-20% share of checkout within US ecommerce, per Bernstein, so a discounted button is a compelling pitch to large merchants. It also still has c.58% of the digital wallets market share, albeit decreasing from c.86% in 2017 (losing share to Apple Pay & Shop Pay).

PayPal is still pretty much a Checkout/Button company:

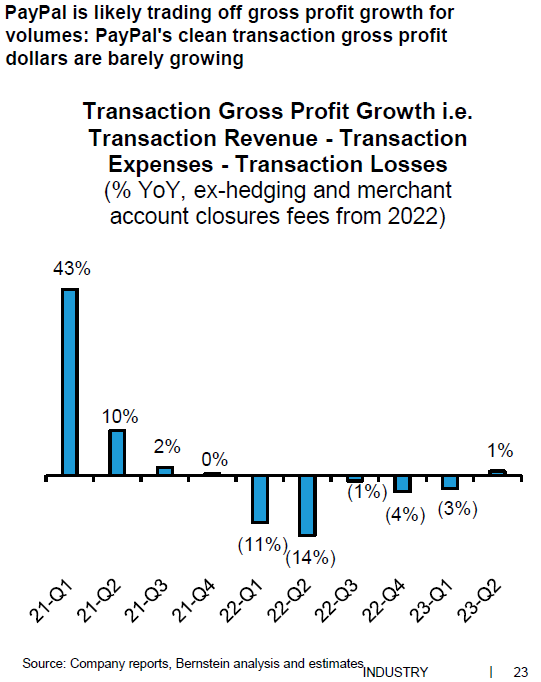

PayPal has likely accelerated these levers in late 2022 / 1H23 to recover the market-share of the Button, which has been underperforming (see below). Apple Pay, Shop Pay, Google Pay, alternative payment methods (e.g., wallets), and better technologies of card-detail-storage enforced by V/MA and payment acquirers are taking share from PayPal.

In addition, PYPL said it would prioritize monetization of value-added services instead of processing, such as FX, in-person payments (omnichannel), and international expansion (i.e., mix of higher TR). I think these aim to balance Braintree’s losses on the processing side. Management has been denying the processing loss strategy publicly despite ongoing transaction gross profit losses (comparable to Adyen’s net revenue definition - see below) and numerous checks from the field that point to that.

I believe those services will not be sufficient to compensate for the losses. FX is, by nature, a tiny piece of an Enterprise acquirer's revenue (<5%), so this is limited at best. In-person is the most challenging piece of payment to crack and differentiate for all types of merchants - many merchants - including much higher quality than Braintree, such as Stripe - have been trying and can’t differentiate from Adyen. International expansion seems the most feasible given the large share still in the hands of very bad acquirers (banks, mostly), and it’s off to a good start. However, the inner product architecture weakness within PYPL prevents it from having an edge over modern / very large-scale acquirers, which is even more critical ex-US where the product is more complex. Also, most countries are not heavy PayPal Button/Wallet users, and interchange rates out of the US tend to be much lower (meaning there’s less opportunity to do discount packages alongside button).

There has undoubtedly been some catch-up from Braintree in the way of grabbing its natural seat as the preferred acquirer of PayPal transactions in domestic volumes where Adyen can’t outperform. Nevertheless, IMO, it should not be viewed as LT durable as a growth driver.

Pricing cuts in the online Enterprise space have had little impact on Adyen’s market share. Fundamentally, payment acquirers are there to deliver 0.5%+ uplifts in revenue while they charge 10-17bps of the same revenue for that. Adyen typically prices higher (e.g., 5-10bps more than competitors) because its product has a higher ROI in most cases. This higher ROI is not in the LSD bps range – it often goes on to deliver 50, 100, 200bps, or higher uplift than the competitor, depending on the case. Discounts in price mean 3-7bps less cost, sometimes 10-12bps lower than Adyen. But at the end of the day, Adyen’s pitch is to deliver much more than that with functionality. Price competition is not new and misses the point of what Braintree (PayPal) is doing. Braintree is, above all, giving up economics on the button.

Pricing has a floor. No payment acquirer can be profitable by pricing Enterprise online transactions at lower than 10-12bps. Every non-Adyen listed payment acquirer can’t sustain a cost base below c10-15bps x its TPV. For example, take Worldpay. In OpEx alone, its costs were $3.5B in 2018 when e-comm was 30% of its revenue -> so assume $1B of online Opex. $600B of online TPV x 10bps = $600MM in revenue (2018). Even with some shared costs with the offline portion, that’s quite far from being decently profitable on $600MM in revenues. The same philosophy applies to every other player. Adyen has the lowest cost base because it’s 100% organic with a lower-cost talent pool, yet it already hit $500MM on costs at this $600B TPV scale.

The only players that can pull the pricing lever to the max are Braintree and Chase. Sustainably, I would say only Chase can. Chase has always priced way below Adyen (sometimes 2-3x lower, sometimes free) because it monetizes the Enterprise with numerous other more profitable financial services. Yet, Adyen (and others) gain a lot of share simply because it delivers much more value than the 10-15bps Chase saves for the merchant on the processing cost/price side.

Chase is still the market leader with >30% of the share simply because there isn’t much that Adyen can do to outperform on Chase-branded credit and debit cards, where Chase uses its acquirer, bank, gateway, and sometimes own rails (i.e. replaces V/MA) for these cards, that can amount >30% of the volumes of a US merchant (meaning that there isn’t much inefficiency in the value chain that an acquirer can address to uplift conversion). However, this doesn’t apply to all Chase-led transactions. As mentioned before, Adyen still has its strengths in certain types of transactions and merchants, but the majority of Chase card transactions are cheaper on an ROI basis to go with Chase processing.

Finally, PayPal Button transactions are limited (15-20% of transactions in the US), so there is a natural cap on how much BT can bundle. For reference, Braintree is already processing the same amount of TPV as the PayPal button.

There is no indication that Braintree has caught up with Adyen on the value side. It still lags in most attributes. Fundamentally, Braintree wasn’t built organically, the team is not as reputable as Adyen’s or Stripe’s, and history has proven that platforms built by M&A and onto the rails of third parties can’t catch up with the leaders even after big reengineering projects (e.g., Worldpay, Chase, examples - and even Stripe to some extent).

Moreover, Braintree doesn’t grab all PayPal button transactions. Adyen delivers much better ROI on “complex flow” transactions, such as subscriptions & omnichannel, and on merchants who work with enterprise-grade integration needed (e.g., Salesforce, Adobe ERPs) or those who like to have a single platform globally.

Key takeaways on pricing are that i) what matters is value, and ii) when there isn’t much value to be delivered, price matters – but fortunately, in the US, this space is limited to Chase-led transactions and, for now, at least, a good portion of PayPal’s turf. This still leaves Adyen with >50% at least of the online market, where it can compete on value.

There isn’t a price war in online payments; There is simply an increased focus on cost, which can be solved with product, not price

The bundle discounting issue seems to be limited to PayPal. All other publicly-listed competitors (see below – digital segments) report healthy take rates (delta in net revs and TPV growth) and plan to deliver healthy net revenue targets in the medium term. Chase (JPM) set an LT plan last year of durable revenue growth on the e-commerce side after years of flat revenue. Industry checks also don’t mention Stripe or any other player cutting prices.

All in all, I believe that the broader issue within the US is the shifting RFP priorities towards speedy cost savings, which fits PayPal’s strategy perfectly, as opposed to a price war scenario.

Four main issues are preventing Adyen from retaining its win rates in the US in the current environment:

Maturing technology stemming from relatively new acquiring and banking licenses: Adyen got its licenses in the US in 2020/2021, which is essential for enhancing the interchange optimization service and overall authorization rates on the pay-ins side as Adyen strengthens its relationship with local banks and rails. However, this takes time as those stakeholders often move slowly to adapt their security rules to a new acquirer. A similar thing happened in Europe, where a former employee said Adyen took 5-7 years to consider itself ready in this sense. Also, over time, as Adyen gets incrementally more scale vs. others, it gets more pricing power from interchange fees vs. other acquirers, increasing its value proposition.

Maturing and under-invested salesforce/accounting management team: Using Adyen’s regional overhead disclosures, I estimate Adyen’s commercial team in the US is still about a third of its European counterpart despite the NAM market being larger than Europe’s. Management called out it would have liked to invest more in the NAM sales team to grow faster in the region, and it plans to do so going forward while reducing the pace of tech hiring globally.

US payments culture: globally, Enterprise payments teams are still slowly evolving from being cost-focused to functionality-driven. A proxy of it is looking at Adyen + Stripe + Checkout's market share on the Enterprise side (non-SMB), which makes up for about 15-17% of the market, I estimate. But that’s from c.5% 7 years ago. Teams are still in the process of treating payments like usual B2B software where the value comes from an ROI evaluation and not necessarily from just the cost. In the US, this trend is even behind. However, secular trends are changing that, such as the rise of platforms, omnichannel, more payment methods, and increased customer conversion challenges.

Sales execution in the short-term: Management hinted it would redirect its salesforce to focus on interchange optimization, which is being prioritized in the current environment. Optimization is basically working alongside the merchant to dynamically prepare the best data packs according to each transaction to send the bank issuers and payment rails so the merchant gets a better interchange fee. I believe Adyen was focusing too much on the functionality piece of the pitch (e.g., payment methods, conversion, customer data, loyalty programs, omnichannel) - teams in NAM were a bit too skewed toward omnichannel per my checks.

“So it's about growing the wallet share that you do with your existing customer base. And in that sense, none of our large customers have left us. So our account management team is in very active discussions with our customer base about how best to help them and some of these interchange optimization routes are some of the projects that get prioritized in this type of environment that they're actively in discussion about.” Adyen CFO, Sept 2023

Adyen’s terminal take-rates should be much higher than what’s implied in the stock because i) online take-rates will fundamentally settle at higher levels than what offline rates settled, and ii) Adyen’s premium service, in most cases, tends to cover peer prices even if they were almost free

The same take-rate compression velocity (proportion to overall TPV growth) of 2023 until 2027 Implies TRs reach c15.8bps in 2027 and c.14.3bps in 2032. At Adyen, TR goes down as volumes per merchant increase following a tiered pricing model.

The pace of take rate allows for steady margin expansion and is close to the breakeven TR of legacy acquirers (c.12-15bps) – it fundamentally can’t go lower than this industry-wide. That’s what happened to the offline Enterprise industry, by the way -> take rates reached a certain level and then stalled at 7-8bps – which is bullish for terminal online TRs; Online take rates need to be significantly higher as online transactions have inherently more room for acquirers to take margin (c.<85pp of online txs are approved vs 95+ for offline; 1-3pp of fraud online vs <0.1pp offline)

Hiring spree is significantly skewed toward tech, of which a good chunk is into new products

Adyen accelerated hiring in 2022, and there is some confusion about why the company is doing it. Management’s message is evident in how the excess people it’s hiring now are geared toward growth creation in the future. They also said that from 2024, Adyen will meaningfully reduce the hiring pace and let the natural operating leverage flow through its long-term target (>65% EBITDA Margin). What’s been miscommunicated, IMO, was the sizable increase in cost per employee, which the Street wasn’t expecting.

What most people are missing here is that the bulk of new hires are tech-related (c.80% of new hires LTM, vs. c.40% usual composition). While management doesn’t directly link them to specific projects, those hires seem to mostly go to the new product verticals (as per LinkedIn). Management has made Platforms & new products the “Phase 2” of Adyen as a company (after spending the first phase at its core processing product) and made a whole investor day last year almost only talking about the piece of the business that is less than 2% of sales currently.

Management also compared this hiring spree with M&A – it told investors to look at it as if it were acquiring another company, but because Adyen does everything organically, the investment is now hitting the P&L and not the CFI. Hence, the best way to look at margin progression is to adopt a hiring curve similar to pre-2022 going forward.

With this in mind, I model a much-reduced pace of hiring: from 1,100 to about 300-400 net new employees per year. This also allows for a Sales Productivity metric (NNARR / year-ago number of commercial employees) that decreases even further from 2023 - much lower than Adyen has seen pre-2023.

Long-term margins seem feasible simply if management lets core margins flow through.

Medium-term base case should incorporate a healthy NRR, flattish NNARR, decaying Sales Productivity, take-rates driven by NRR trends (i.e., decreasing following the historical pace vs. NRRs), and margins getting back to normal; 5-year high-teens IRR seems achievable

As I said, Adyen is still outgrowing the addressable market by a wide margin. Its market share is still c.10% worldwide (c.20% OUS ex-China, c.5% US), and legacy acquirers still make up for c.70-80% of the market.

Base case algorithm:

End market growth: c.9% CAGR

2027 Online market-share: c13% overall online (c.8% US, c.24% OUS ex China); Terminal Online market-share: c17% overall; c17% Online TPV CAGR

until 2027

POS market-share: <3%; I’ve estimated that the wallet-share on existing POS merchants is c.20% - so, a c.30% POS TPV CAGR (my base case) means the penetration goes to c.30-35% in 2027; This is reasonable because most Adyen omnichannel contracts are set for >70% of the volumes, so there is a high degree of conservatism embedded in, especially as the company keeps winning very large new logos that can make penetrations low for a very long time

2022-2027 c19% Total TPV CAGR

Net revenues c.17% CAGR (vs. 3-5y guidance of mid-20 to low-30s CAGR)

c.54% EBITDA Margin 2027

FCF c.22% CAGR (expense SBC & considers lease payments)

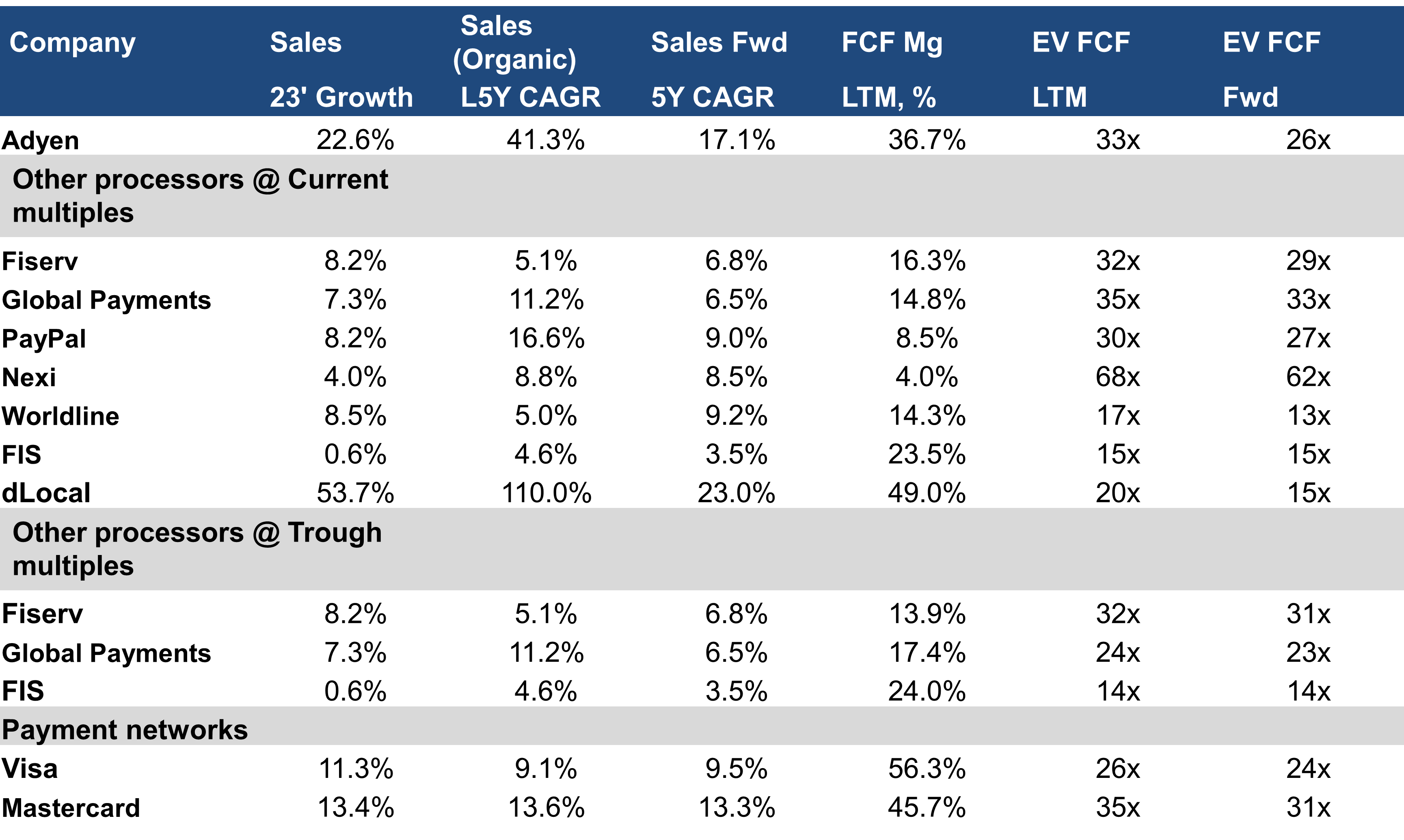

Exit multiple of 26x EV/FCF (from c33x at entry) – DCF-implied multiple @ 10% cost of equity, 4% perpetuity growth, 15% assumed terminal ROIC (from 127% ROIIC in 2032)

2027E IRR of c18%

Zero contribution from new products. Adyen is working hard to deliver its work on Issuing, Platforms, and Embedded Finance (I think it could reach 10-15% of Adyen’s revenue in 5-10 years). I assume 0 because everything is still pretty much in pilot phase.

Implied global online full-stack market-share projection:

Key financials:

All in all, I think the company is on the verge of inflecting its (very high) ROIIC and stabilizing the NNARR (even conservatively assuming decaying levels of sales productivity) from 1H24 as margins come back up and salesforce matures, and its valuation should stabilize as the market sees continued share gains at premium take-rates.

This exit multiple is a bargain relative to how legacy acquirers (much worse businesses, with much lower growth and returns on capital) trade currently and vs. the last trough multiples of 2022 (see below). Caveat: these are multiples on FCF ex-M&A – if we include M&A, legacy acquirer’s multiples would get a 30-50% haircut!

Quality caveat

Adyen is a high-quality business but doesn’t score max due to a few things. It won’t likely deserve a high-20s/30x FCF multiple on HSD growth. At a similar growth level, Adyen will be more sensible than V/MA to downturns (that trade at these levels) because it has less pricing power than the networks, which largely stems from extremely high switching costs. Adyen is forced to surf the underlying drawdown of its customers and can’t push for price increases because clients will seek easy ST gains by switching to lower-cost providers. While Adyen can reach a level of value superiority one day that it can start above-inflation hikes, it still doesn’t happen and is much less predictable than the fact that we know, for sure, that consumers won’t stop paying by cards or wallets (V/MA) in most scenarios, hence Adyen’s lower multiple. Adyen will still outperform the economy because its customers grow way more than the GDP, but it won’t be a company that will post LSD-MSD headline sales increases through price. Further, because there are way more competitors in the acquiring vs. the networking space, Adyen’s position is more fragile.

Downside seems limited over the long-term, but the stock can further de-rate depending on whether 2H23 results keep the current bear narrative unchanged

Long-term, I can imagine two reasonably possible bad scenarios: 1) ONLINE market-share pace could run at half the levels due to stronger competition, but at current take rates -> IRR goes to c.9% at 24x EVFCF (Adyen would still be growing c10% TPV 5y out from 2027), @ EBITDA Margin of 47% 2027 (largely unchanged from 2023); or 2) ONLINE market-share pace running at base case levels but at weaker take rates stemming from stronger competition, going faster endgame (c12bps in 2027) -> 9% IRR as well.

Lose-money scenario would be where Adyen both drastically decelerates market-share gain pace online AND take-rates suffer from competition on the value side, AND its offline arm also meaningfully decelerates to low to mid-teens growth fast -> In this scenario, 5-year IRR would be -2%.

While the above is a very unlikely scenario, I acknowledge that any further deterioration in the next half could make the market extrapolate narratives like this for the LT, and the stock could very well de-rate from 33x to c20-25x. It’s possible, especially as consensus numbers remain optimistic for 2024 and 2025. There is quite a detachment in estimates & quality perception between the sell-side and the buy-side (stock-implied expectations & my personal checks) on this stock.

However, 20-25x isn’t even where Fiserv, GPN, or PYPL trade today (or have mostly traded in the past). Also, GPN’s trough multiple last year reached 24x, but consensus had LSD growth going forward. It would take a lot to make Adyen grow profits LSD.

I think those bear cases are balanced with Adyen’s new product potential to some extent, which can add 3-5% of revenue growth per year. Adyen could also very well ramp up more rapidly on the offline side (trillions of TAM) and significant online wins recently (Shopify and Amazon).

Next catalyst will be the Investor Day in Nov 2023 where the CEO will “better explain the source of confidence” in Adyen’s growth potential. Adyen’s IDs are not usually very helpful for investors, but this time, it can be different given the share price weakness. Next results will be only in Feb 2024.

Recommendations I would give to management:

Start reporting net revenue & TPV retention rates, as dLocal (DLO) does

Detail how many of the team members are working on the new products so investors can get a better view of the underlying economics; Perhaps regional economics as well

Give investors KPIs to track the progression of the attach rates of new products, sales productivity metrics, and the number/maturity of quota-bearing sales reps

Buy (more) stock!

< Disclaimer >

This material is provided solely for informational purposes and is not tailored to any recipient, and is not based on, and does not take into account, the particular investment objectives, portfolio holdings, strategy, financial situation, or needs of any recipient. As such, any advice or recommendation on this website may not be suitable for a particular recipient. You must make your own independent decisions regarding any securities or financial instruments mentioned herein. The fact that the writer has made available to you through the website, investment opinions, and other information constitutes neither a recommendation that you enter into a particular transaction nor a representation that any financial instrument is suitable or appropriate for you.

Information herein presented may be sourced from third parties and public filings. Any links, screenshots, and mentions to these sources are included for convenience only and are not endorsements, sponsorships, or recommendations of any opinions expressed or services offered by those third parties.

Thanks this is a very thorough and insightful writing.

I do have two question though:

1) I see some comments referring that Braintree's accelerated growth are not about price cutting but through better authorisation rates e.g. more advanced technology adoption such as Payment tokenization. Do you think this could factor more in their recent share winning? After all both PayPal's former CEO and CFO have claimed that they did not aggresively lower the unbranded rates, which negates some analysts' view.

2) In your comparison of Braintree vs Adyen full-stack growth, why do you adjust the number of PPCP effect out? Because it seems like this part revenue from platform prove to be very important for Braintree and they plan to grow with it much more in the future.

Thank you.