Overall Payments Performance Is Worsening & Acceptance Rates are Declining, say Checkout & Oxford

Overall Payments Performance Is Worsening & Acceptance Rates are Declining, say Checkout & Oxford

Counter-intuitively to many, the 2nd edition of a research paper on payments indicates that the room for optimizing payments is far from narrowing.

We have watched Adyen, Stripe, Checkout, and other providers outgrow the legacy payment processors for many years. The market share for these guys grew from c.12% in 2019 to c.20% in 2022, mostly stealing from players like Chase, Worldpay, and First Data.

That would leave us thinking that the inefficiency in the payment chain is decreasing overall. As those modern processors gain share, the problems in the payment chain are probably reducing. The fact they have a higher market share now must mean, on average, that there is less inefficiency to be solved.

Some argue that as the market becomes increasingly efficient over time, there will be less and less opportunity for a company like Adyen to profit from payment inefficiencies. Consequently, Adyen may experience greater pricing competition and a weakening moat as it gains more market share.

A “bear” corollary to the above - from a wise friend at one of the largest long-only funds - goes about saying that, as the legacy processors catch up with easier-to-develop payment features, such as i) alternative payment methods, ii) automated retries, and iii) global-local processing, they will be more prepared to close most of the inefficiency gap in the acquiring-gateway value chain, which will make the Adyens of the world only sustain a single-digit-bps price advantage vs. the 10-20bps+ seen currently.

I think those arguments might only be valid if you consider that the levels of inefficiency are static (and that the legacy players would implement those easier-to-develop features well - debatable, but let’s leave this discussion for another time).

However, key people in the payments world have been putting this assumed inefficiency inertia into question - indicating that we are seeing a rising complexity of payments and, instead, increased inefficiency. An increased number of payment methods & cross-border operations, increased regulation, complex network implementations, and poor issuer adaptability to innovation have been cited by experts as the main factors of increased complexity. Adyen has notably been pounding the table in the last years that payments are getting more complex, year after year, which increases customer appetite for modern processors. Yet, it’s difficult to quantify and track the “complexity levels” in the payments world to ensure what is seen on the ground.

Not until now, it seems: Checkout.com is the first (at least I know) to publicize some data / KPIs that attempt to track complexity and levels of payment technology adoption. The company publishes that in periodic reports. The first edition was in 2021, and last month, it released the second edition (High-Performance Payments: The hidden billion-dollar opportunity), with a more complete overview, in collaboration with Oxford Economics.

In short, the report says that the overall payment performance seen by merchants is worsening.

It means there is more room to generate value as an acquirer in 2022 than in 2019 - even with the rise of modern platforms. The complexity increased so much that the overall baseline inefficiency levels deteriorated way more than what Adyen, Stripe etc. could solve. So, if we consider that these overall worsened levels (see below) include Adyen, Stripe etc., then the ex-Adyen, Stripe piece deteriorated way more than the overall reported by Checkout!

You can download the report here. Of course, taking it with a grain of salt is essential because it comes from a payments provider (even though it’s done in collab with Oxford). However, it resonates a lot with what stakeholders are saying, with the degree of share loss by legacy players, and the overall fraud / cyber-crime insurgence (which prompts constant changes in security / fraud policies by issuers and networks). So, it doesn’t surprise me that much. The reasons Checkout lays out for why it is happening also make sense.

Here are the highlights:

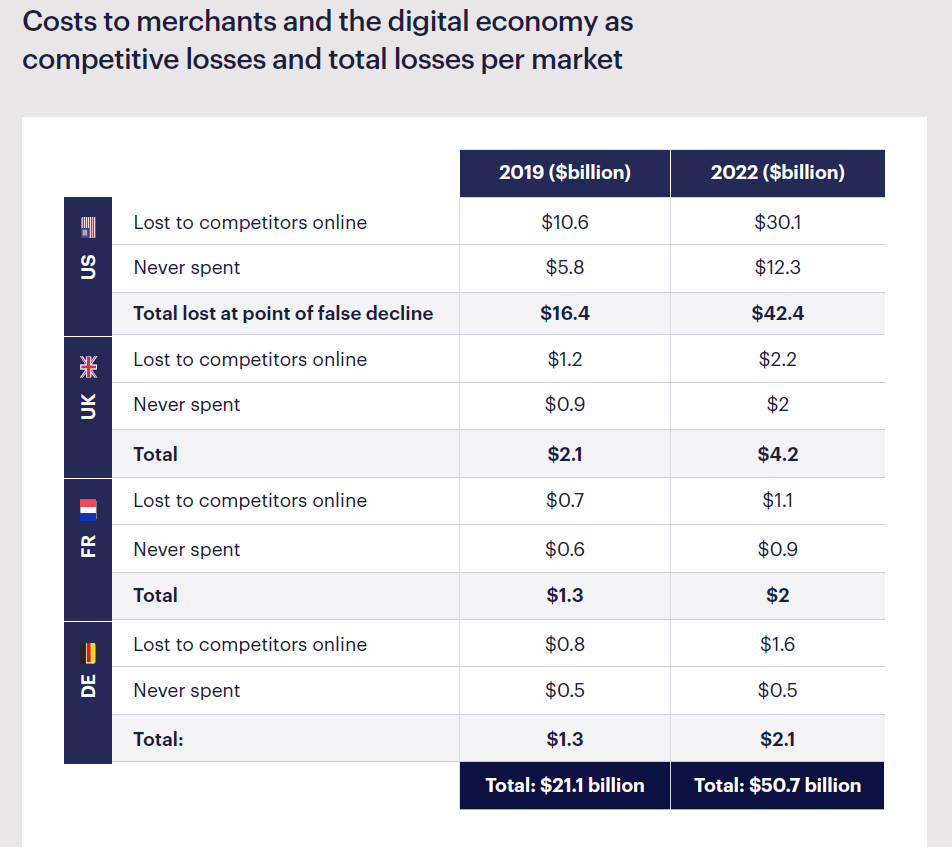

$50.7B was lost in the US, UK, FR, DE solely due to falsely declined payments, up from $21B recorded in 2019 – a growth rate of 140%, far outpacing the c.30% growth in online volume in the same period. Most of those losses by merchants are lost to their competitors thereafter (because the customer will try to buy the same thing on another website / app). Breakdown:

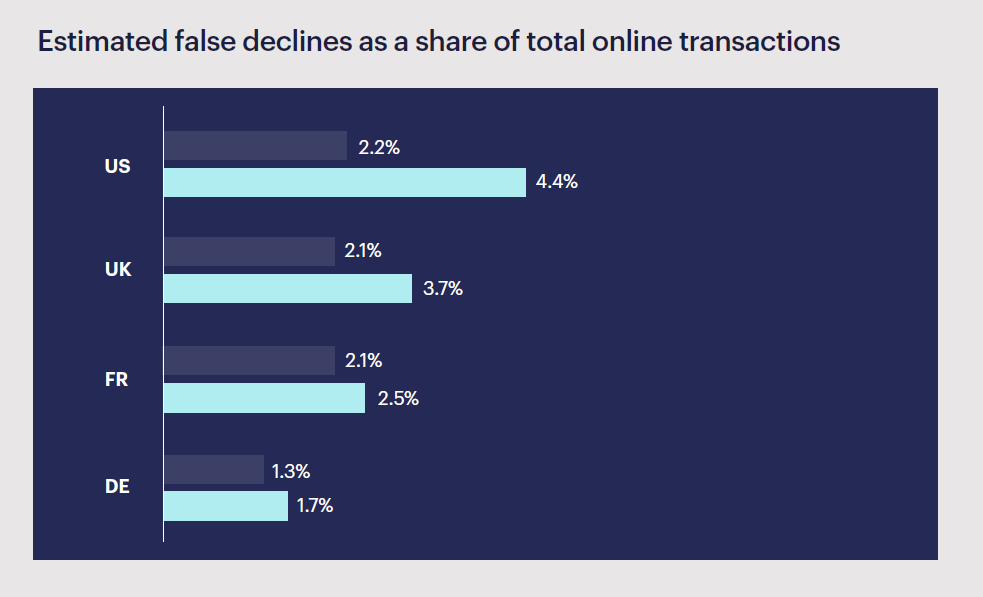

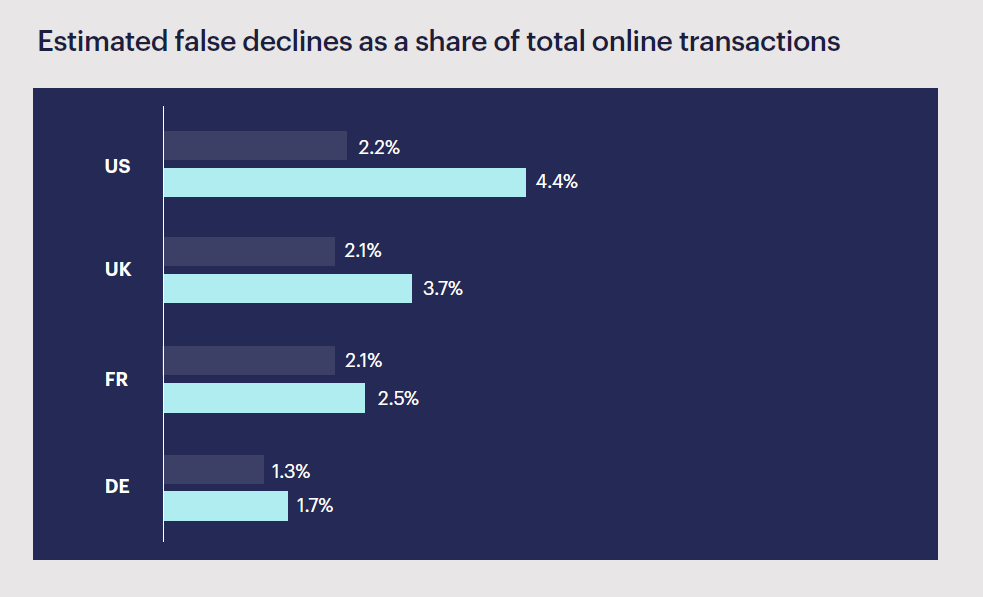

False declines rose from 2019 to 2022. The US leads with the highest rate of false declines (even with Chase and PayPal verticalizing a great deal of the payments chain in c.30-40% of the volumes!) Legend: Dark blue = 2019, Light blue = 2022

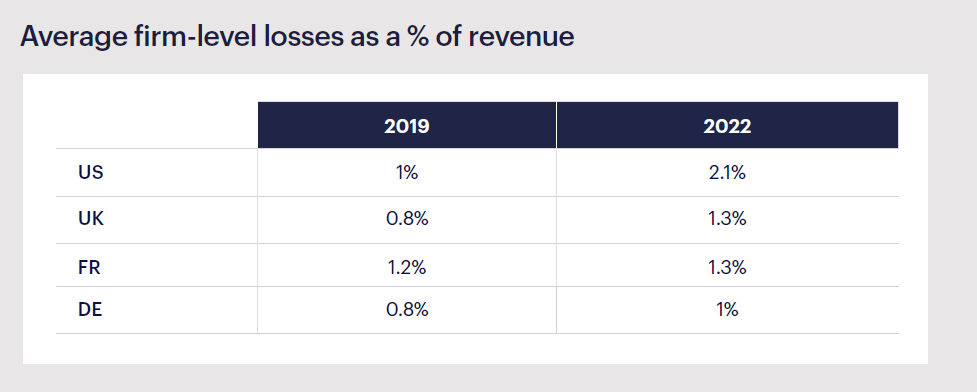

Businesses lost between 1% and 2.1% of their revenues (in 2022) due to inadequately optimized payment acceptance. Rising from 2019. By region:

Online payment fraud is rising fast. In 2021 alone, it increased by 285%. it’s estimated online sellers will experience losses exceeding $206 billion between 2021 and 2025. One of the biggest trends is increased automated attacks, primarily through bots. These attacks make it easy for fraudsters to scale their efforts. For example, it can cost less than $200 to attempt 100,000 account takeovers, with a success rate between 0.2 to 2%.

Consumer highlights1:

45% of consumers say they don't retry payment following one false decline

15% of consumers surveyed said they used a new payment method for the first time in 2021

Main reasons why false declines are rising:

Rise of cross-border payments: “payments performance is hampered by a lack of access to local payment methods and currencies, excessive interchange fees, and a lack of access to local acquiring which can lead to unnecessary false declines as well as driving up fees associated with cross-border payments.”

Regulation: “Inevitably regulators have had to keep up with the pace of growth and change in online payments and that includes addressing the new fraud risks. In particular Strong Customer Authentication (SCA) and 3D Secure (3DS and 3DS2) have added palpable friction to the payment process compounded by risk assessment failures which trigger further false declines.”

Disjointed scheme and issuer rules (especially problematic with the rise of Network Tokens): “Each of the payment schemes – such as Visa, Mastercard, and American Express – has their own varying rules, but they have all been leaning

more and more towards the use of Network Tokens rather than Permanent Account Number (PAN) details on card payments. In theory, the introduction

of Network Tokens provides merchants the opportunity to lower processing costs and drive higher acceptance rates. Nevertheless, the deployment of Network Tokens is not accepted uniformly by issuers and so a dynamic approach is required. Merchants remain ill-equipped to provide the required information with reactive flexibility, leading to excessive false declines and missed cost-saving opportunities.”

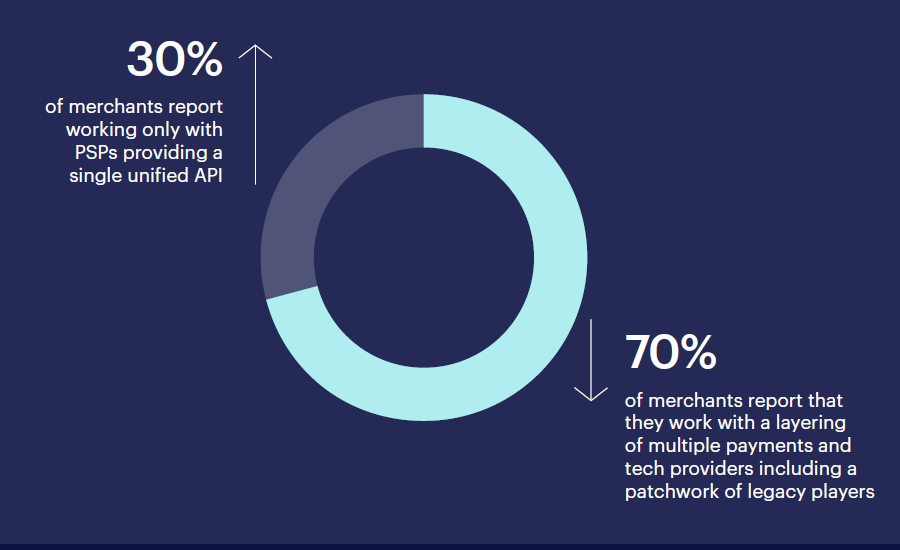

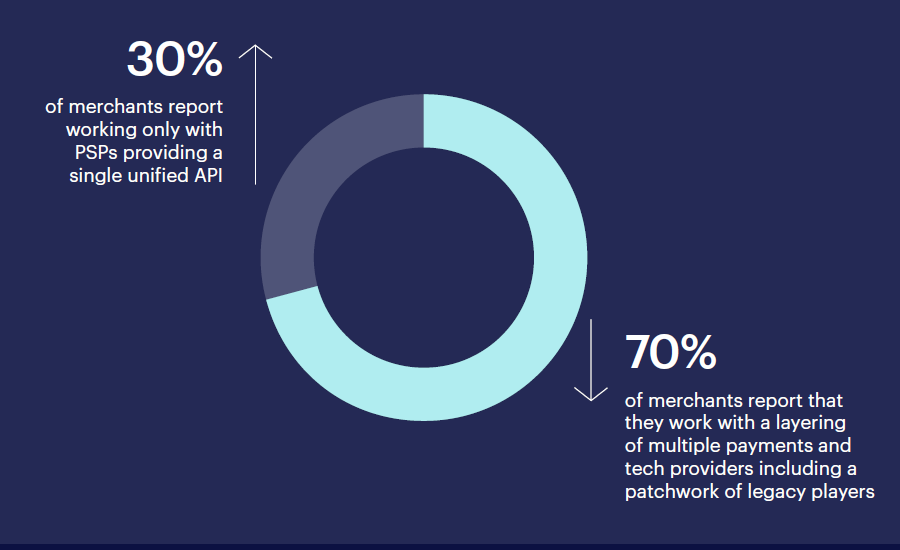

Disjointed tech stacks and a dearth of data: “Some 70% of merchants surveyed2 report having disjointed payments tech stacks composed of legacy players layered with some newer tech vendors, each responsible for a different part of the puzzle. This quickly leads to ‘black boxes’ where important payments data is neither transparent, nor is it pulled through in order to drive optimal results.”

Evolution of survey data: room for increased payments performance remains incredibly large!

“Optimal payments acceptance may indeed be table stakes. But doing it well is far from simple.”

For more on Adyen and payments, check my latest posts and subscribe.

n = 8,000 consumers.

n = 1,500 medium to large enterprise merchants.